Understanding Guardrails: A Strategy for Retirement Longevity

Introduction

Planning for a 30-year retirement can feel overwhelming. This post examines the use of mathematical models to simulate portfolio longevity and the effects of market volatility over a 30-year horizon. It evaluates a strategy designed to sustain consistent annual withdrawals, inflation-adjusted, through the application of dynamic "spending guardrails" and systematic withdrawal rules.

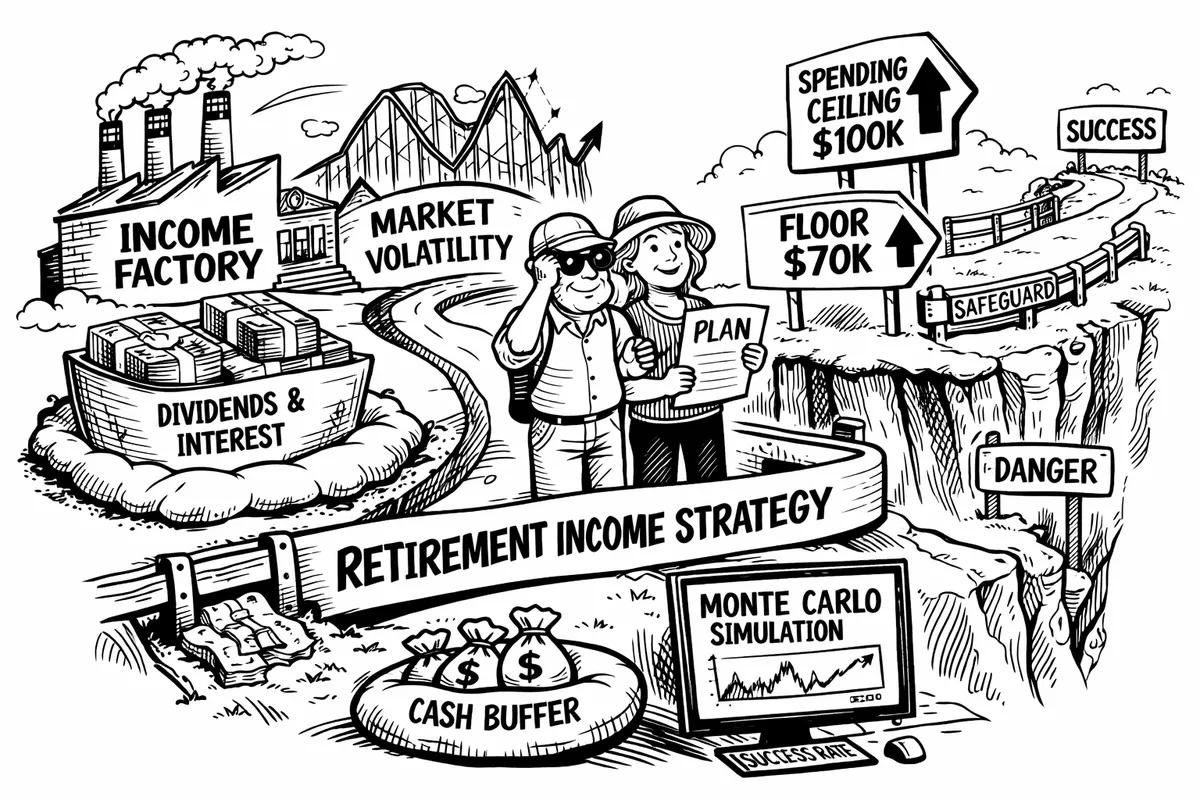

The Core Rationale: The "Income Factory"

The "Income Factory" concept is a theoretical framework where a portfolio is modeled to prioritise dividends and interest over the sale of underlying assets.

For the purposes of this simulation, the following arbitrary asset classes were selected to test the logic of the model:

- Australian Shares (30%): Selected for growth potential and tax-effective dividends.

- International Shares (40%): These provide exposure to global growth and help diversify risk.

- Australian Bonds (30%): These act as a stabiliser, providing steady interest and a cushion when the stock market is volatile.

These percentages are used as a baseline for the simulation and do not represent a recommended asset allocation for any individual.

Protecting Against "Sequence of Returns" Risk

Sequence of Returns risk occurs when a major market crash coincides with the beginning of retirement. If a model requires selling shares at depressed prices to meet income targets, it can lead to a 'capital depletion' effect that is difficult to reverse, even if the market later improves.

To combat this, the plan uses two key defenses:

- The Cash Buffer: This simulation incorporates a dedicated cash reserve, initially set to cover three years of projected outflows. When simulated dividend yields fall below the target, the model draws from this buffer, avoiding the necessity of liquidating equity assets during market downturns.

- Spending Guardrails: This is a flexible approach to spending.

- The Up-Years: In this model, the simulation is programmed to increase spending during "Up-Years" and reduce spending by 5% during "Down-Years" to test the impact of flexibility on the portfolio’s survival.

- The Down-Years: If the portfolio has a negative year, the inflation raise is skipped and spending reduced by 5%, down to a "floor" value. This small adjustment significantly reduces the strain of the portfolio during lean times.

How the Simulation Works

- To test if this plan actually works, we use a Monte Carlo simulation. Think of this as a "stress test" that runs 1,000 different versions of the future.

- In each version, the computer randomly assigns different market returns and inflation rates for every year over a 30-year period. Some "futures" are great, with booming markets, while others are difficult, with multiple crashes or high inflation. By looking at the results of all 1,000 scenarios, we can see the Risk of Ruin - the percentage of times the portfolio completely ran out of money.

What Makes a Plan "Robust"?

In professional financial planning, a plan is generally considered robust if it has a Risk of Ruin of 5% or less (meaning it succeeds in 95% of simulated futures). Some models aim for a 90% success rate as a baseline. The objective of the simulation is to identify conditions that offer a high statistical probability of sustainability, ensuring the modeled lifestyle can be maintained across a wide range of economic environments.

Conclusion

This simulation suggests that systematic withdrawal rules and flexible spending may have a greater impact on portfolio longevity than asset selection alone. By combining a diversified portfolio with a cash buffer and flexible spending guardrails, one can explore creating a "weatherproof" model that can navigate the ups and downs of the next 30 years with confidence.

References & Further Reading

The 4% Rule & Safe Withdrawal Rates: Determining Withdrawal Rates Using Historical Data

The original 1994 study by William Bengen that established the benchmarks for portfolio longevity.Dynamic Spending & Guardrails: Decision Rules to Maximize Retirement Spending

Research by Guyton and Klinger on how "guardrails" can significantly increase the safe amount you can spend.Sequence Risk Management: Understanding Sequence of Returns Risk

This section examines how the specific sequence of market returns—especially during the initial years of the withdrawal phase—can fundamentally impair capital preservation. It demonstrates that early losses can lead to permanent portfolio depletion, even if the long-term average annual return appears favourable.Current Market Benchmarks: Morningstar’s State of Retirement Income Report

Updated annual research on safe withdrawal rates based on today's interest rates and stock valuations.

Disclaimer: I am not a financial adviser. This blog is a personal project documenting my own research and simulations. The figures and strategies discussed (such as the 30/40/30 split or the $80,000 income target) are hypothetical examples for illustrative purposes only and do not constitute financial advice. Australian financial laws are strict; please consult an ASIC-licensed financial planner before making any investment decisions.